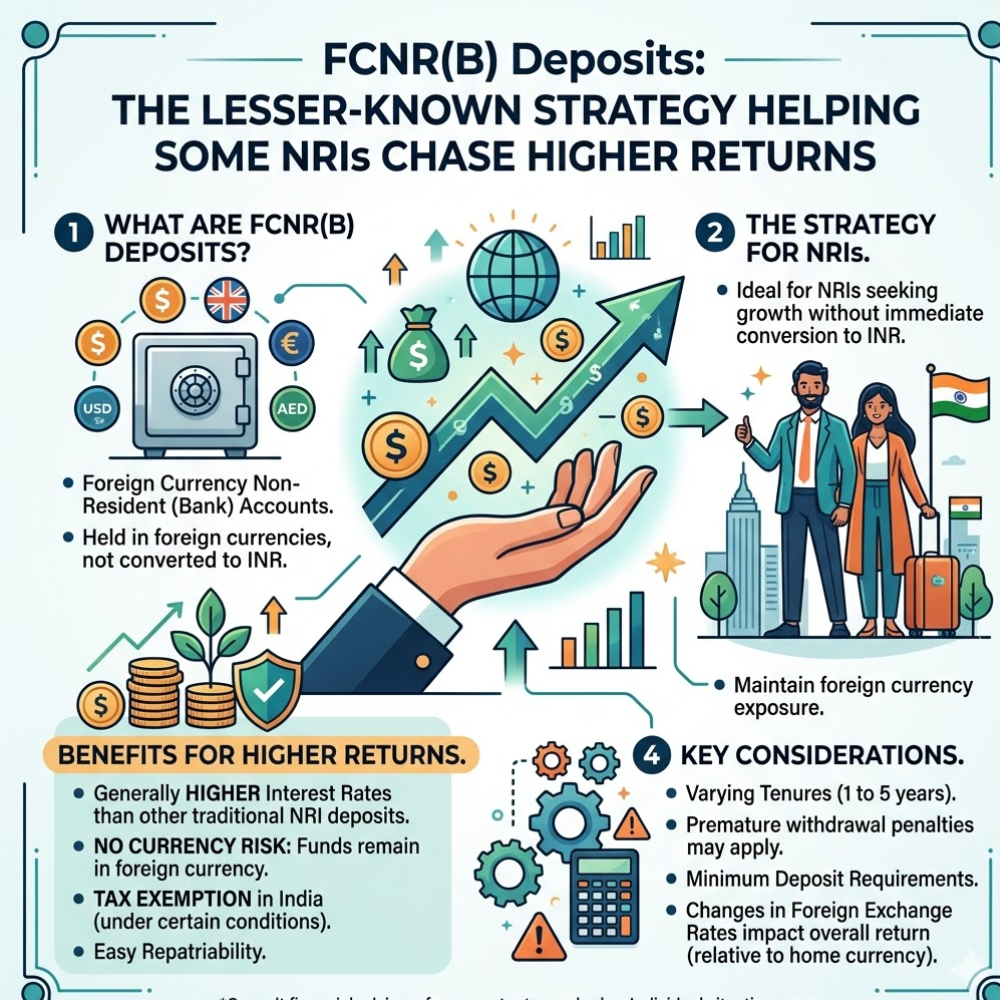

FCNR(B) Deposits: The Lesser-Known Strategy Helping Some NRIs Chase Higher Returns

For a long time, Non-Resident Indians (NRIs) looking to gain steady returns on their investment funds have depended on commonplace choices such as abroad settled stores, reserve funds accounts, bonds, and value speculations. Be that as it may, a later advancement in India’s keeping money segment has brought a moderately specialty speculation item back into the spotlight—Foreign Cash Non-Resident (Bank), or FCNR(B), stores. More imperatively, it has opened the entryway to a technique that might possibly offer assistance a few NRIs gain altogether higher returns than conventional deposits.

At to begin with look, FCNR(B) stores are direct. They permit NRIs to stop cash in remote monetary standards such as the US dollar, British pound, euro, Australian dollar, or Canadian dollar with Indian banks. Since both the foremost and intrigued are kept up in the same outside money, financial specialists are secured from vacillations in the Indian rupee. This highlight has continuously made FCNR(B) stores appealing for abroad Indians who need presentation to Indian banks without taking cash risks.

What has changed as of late is the Save Bank of India’s choice to resuscitate a uncommon swap window that altogether diminishes the supporting costs ordinarily borne by banks. As a result, numerous banks have strongly expanded the intrigued rates they offer on FCNR(B) stores, with a few teach presently advertising returns over 6% and, in certain cases, indeed crossing the 7% mark.

For NRIs acclimated to seeing dollar-denominated fixed-income ventures abdicate much lower returns in created markets, these rates are troublesome to ignore.

Why FCNR(B) Stores Are All of a sudden Attractive

To get it the fervor, it is imperative to get it how these stores work.

Traditionally, when Indian banks acknowledged dollar stores from NRIs, they had to fence the cash hazard since they would change over those dollars into rupees for loaning exercises. Supporting included costs that diminished the intrigued rates banks might manage to offer. Concurring to managing an account industry gauges, these costs frequently extended near to 3% annually.

The RBI’s most recent move viably expels much of this burden for banks, empowering them to pass on higher returns to contributors. A few major loan specialists have as of now reexamined their FCNR(B) rates upward, making these stores significantly more competitive compared to comparative items accessible in nations such as the Joined together States, the Joined together Kingdom, and Canada.

For numerous NRIs, basically locking stores into a high-yield FCNR(B) store can be a sensible way to produce unsurprising pay whereas maintaining a strategic distance from exchange-rate uncertainty.

However, a few speculators are investigating an extra layer of strategy.

The Use Opportunity

The lesser-known approach includes utilizing leverage.

In straightforward terms, use implies borrowing cash to contribute a bigger sum than one may utilizing individual reserves alone. Certain well off NRIs with get to to low-cost borrowing offices overseas are considering credits in outside money and at that point contributing the borrowed reserves into higher-yielding FCNR(B) stores in India.

Imagine an speculator who can borrow dollars at 5% yearly and contribute those dollars in an FCNR(B) store yielding 7%. The spread between the borrowing taken a toll and the store return makes an opportunity for benefit. When use is included, indeed a humble contrast between the two rates can result in a altogether improved return on the investor’s claim capital.

Some budgetary examiners appraise that beneath great conditions, utilized FCNR(B) ventures may produce returns that take after those customarily related with value ventures or maybe than fixed-income products.

Naturally, such projections have created impressive intrigued among high-net-worth NRIs.

But as alluring as the numbers may show up, use is never free of risk.

The Dangers Behind the Strategy

One of the greatest misinterpretations encompassing utilized FCNR(B) contributing is that it is a ensured benefit opportunity.

In reality, a few factors can influence the outcome.

The to begin with chance is borrowing fetched. Intrigued rates on advances can alter over time, particularly if the borrowing is connected to floating-rate benchmarks. If borrowing costs rise whereas store returns stay settled, the anticipated benefit edge can recoil substantially.

The moment concern is liquidity. FCNR(B) stores ordinarily come with settled residencies extending from three to five a long time. Speculators may confront punishments or decreased returns if they require to pull back reserves some time recently development. In the interim, credit commitments proceed in any case of advertise conditions or individual money related circumstances.

Taxation is another imperative calculate. Whereas intrigued earned on FCNR(B) stores is by and large absolved from assess in India for qualified NRIs, assess treatment in the investor’s nation of home may vary. Depending on nearby directions, returns may be subject to tax collection abroad, possibly decreasing the genuine advantage of the strategy.

There is too counterparty hazard. In spite of the fact that Indian banks are firmly controlled, concentrating a expansive sum of borrowed cash into a single venture vehicle is once in a while without concerns.

Finally, use itself amplifies results. Whereas it can boost picks up, it can too open up misfortunes if suspicions fall flat to materialize as expected.

Who Ought to Consider It?

The utilized FCNR(B) methodology is not appropriate for each NRI.

It tends to request more to advanced speculators who have get to to low-cost borrowing, a clear understanding of cross-border assess suggestions, and the budgetary capacity to retain potential difficulties. For such people, the procedure may frame a portion of a broader wealth-management arrange or maybe than serving as a standalone investment.

On the other hand, normal speculators may discover that the conventional utilize of FCNR(B) stores as of now offers adequate benefits. Tall intrigued rates, assurance from cash vacillations, and relative effortlessness make these stores alluring indeed without any use involved.

A Window That May Not Remain Open Forever

The current eagerness encompassing FCNR(B) stores is connected to a extraordinary RBI office that remains accessible as it were for a constrained period. The window is pointed at drawing in remote cash inflows and fortifying India’s outside position. Comparable measures were utilized in the past amid periods when policymakers looked for to boost remote trade reserves.

As a result, the abnormally tall rates as of now accessible may not stay in put indefinitely.

For NRIs assessing their venture choices, this makes FCNR(B) stores worth analyzing sooner or maybe than later.

Conclusion

FCNR(B) stores have unobtrusively developed as one of the most talked-about openings for NRIs in 2026. Rising intrigued rates and steady approach measures have changed what was once a specialty managing an account item into a possibly fulfilling venture road. Whereas a few speculators are investigating use to improve returns advance, the procedure comes with important dangers that ought to not be overlooked.

For most NRIs, the more intelligent approach may essentially be to take advantage of the moved forward store rates without including the complexity of borrowed cash. After all, protecting capital whereas winning alluring returns remains the essential reason of fixed-income contributing. The later FCNR(B) boom may offer energizing conceivable outcomes, but as with any monetary opportunity, understanding the dangers is fair as imperative as chasing the rewards.